Rachel Zazzera's Blog

DRE#01925193

DRE #01885775

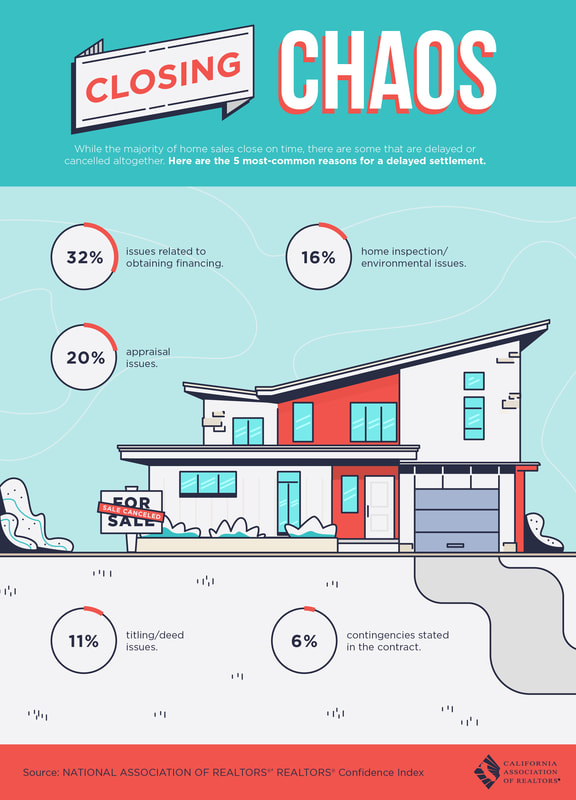

Top 5 Reasons For Not Closing Escrow On Time- Rachel ZazzeraNo real estate transaction is perfect and no matter how smoothly you think the process may go, there is usually some kind of hick-up along the way. Many of the problems will be out of your control, but almost always, there is a way to make everything right.

Here is a list of the top 5 common problems when it comes to closing the deal: 1. Financing- It is always important to get pre-approved when getting ready to shop for a home. This is important to for many reasons but mainly to see what you can afford and to show sellers that you are a serious/ready buyer. With a pre-approval, the lender collects a lot of information about you to obtain the amount you can afford. Some of these items include W-2's or any other income for the past 2 years, copy of bank statements, etc. Even after collecting all of this information, once you get into an escrow, there are other things that come up that the lender asks for. The lender receives a copy of the contract that you submit to the seller, and based off of the contract, the lender may need additional information or have issues with what is written in the contract. Most of the time, the issues related to financing occur at a point while you are in escrow and not during the initial pre-approval process. 2. Appraisal- Another part of the financing issue specifically deals with the appraisal value. When taking a loan on a home, the lender will always require an appraiser to inspect the home and give their opinion on the value. In a market like we are experiencing today, buyers are continually placing bids on homes that are extremely over the asking price and in some cases, over the homes value. When appraisals come in lower than what the agreed purchase price is on the home, lenders will not lend the full purchase price. The lender will only lend up to the appraised value. It will be up to the buyers to come up with the difference in appraisal value and offered purchase price. This is normally very difficult to do, because this amount is on top of the amount of money the buyer is already putting down (i.e. 20%, 10%, etc). 3. Home Inspection- A home inspector checks the entirety of a home at the surface level and gives a general idea of any issues that they may find. This meaning, a home inspector is not an expert on all things that a home is made of. Example, if the home inspector thinks the roof of a home is slightly aged, he/she will state in the report that a roof contractor will need to give their own opinion. Once the home is checked out and the buyers are ready to submit their "request for repairs", it is difficult to come to an agreement between buyer and seller as to what the sellers will fix and/or give credit for. 4. Title- In California, a title report is always requested and should be investigated by all parties to the transaction. The title report shows if there are any liens on a home, who actually has ownership of the home, any easements on a property, etc, etc. A buyer will want to make sure the title report comes out clean (all liens paid off, the actual owner signing off on the purchase agreement) prior to taking ownership of the home. 5. Contingencies- There is a count down of days for buyers to perform their due diligence to see if they actually want to proceed with purchasing a home. Contingencies include but are not limited to: inspection, appraisal and loan. All contingencies need to be removed prior to closing escrow. If buyers fail to remove any one contingency, it can hold up the close. Buyers would normally remove contingencies after certain expectations are met (i.e. the buyer performs all inspections, the appraisal comes back at the purchase price, and the loan clears with no conditions).

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Archives

October 2020

Categories

All

|

RSS Feed

RSS Feed